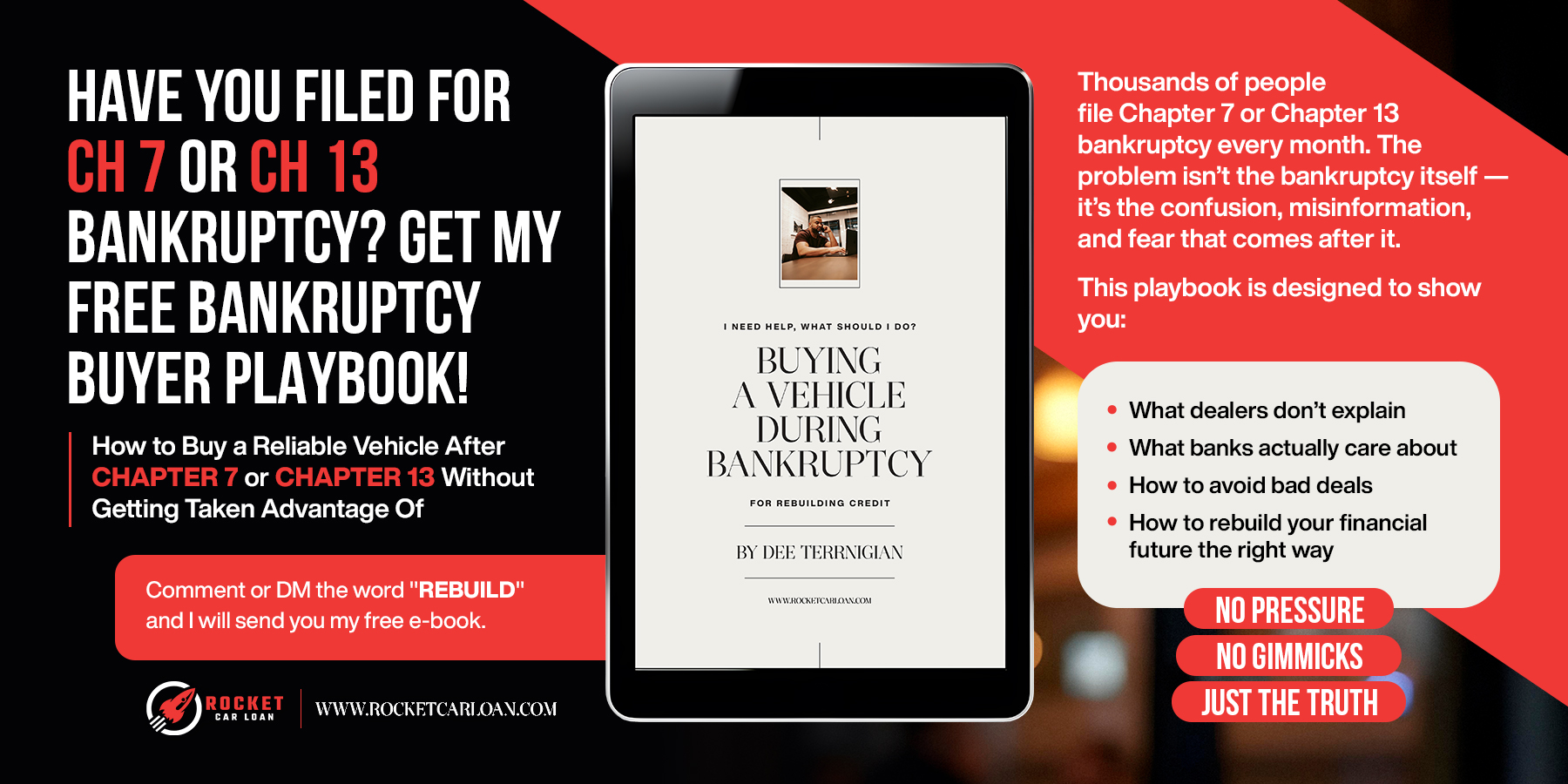

THE BANKRUPTCY BUYER PLAYBOOK

How to Buy a Reliable Vehicle After Chapter 7 or Chapter 13 — Without Getting Taken Advantage Of

INTRODUCTION

If you’re reading this, you’re not alone — and you’re not broken.

Thousands of people file Chapter 7 or Chapter 13 bankruptcy every month. The problem isn’t the bankruptcy itself — it’s the confusion, misinformation, and fear that comes after it.

This playbook is designed to show you:

What dealers don’t explain

What banks actually care about

How to avoid bad deals

How to rebuild your financial future the right way

No pressure. No gimmicks. Just the truth.

This is meant to replace the noise with a simple, step-by-step framework so you can make decisions from a position of clarity instead of stress.

After a filing, the stakes are higher because one bad move—an inflated payment, the wrong term, a high-mileage vehicle that triggers repair surprises, or a loan structure that traps you in negative equity—can turn “starting over” into a longer setback.

The goal here is to help you understand how approvals really work, how lenders interpret stability, and how to choose a deal you can comfortably maintain long enough to create meaningful progress.

When you know what to prioritize and what to avoid, you stop gambling with your credit and start building measurable momentum—stronger payment history, improved lender confidence, and a realistic path to better rates and better options over time.

SECTION 1:

THE BIGGEST MYTHS ABOUT BUYING AFTER BANKRUPTCY

Myth #1:

“I have to wait years to buy a car."

➡️ Reality: Many lenders approve buyers during or immediately after bankruptcy.

Myth #2: “All post-bankruptcy loans are bad deals.”

➡️ Reality: Bad deals come from bad guidance — not your situation.

Myth #3: “My credit score is all that matters.”

➡️ Reality: Income, stability, and structure matter more than the number.

These myths keep people stuck because they sound logical, but they push borrowers into the worst possible mindset—either waiting without a strategy or jumping at the first “yes” out of fear.

The truth is that approvals after bankruptcy are often more about context than time: the lender wants to see that the financial bleeding has stopped and that your current situation is stable, which is why verified income, consistent residence, realistic monthly obligations, and a sensible vehicle choice can matter more than the date on the discharge paperwork.

Likewise, post-bankruptcy financing isn’t automatically predatory; the difference between a deal that helps and a deal that hurts is usually the structure and who’s guiding it—whether the payment is truly affordable, whether the term and vehicle risk are aligned, and whether the loan is positioned with a lender whose guidelines actually fit a rebuild profile.

And while the score is part of the picture, it’s rarely the decision-maker by itself: two people with similar scores can get completely different outcomes depending on stability, ratios, and whether the deal was designed to succeed over time rather than merely “get bought.”

When you replace myths with a plan, you stop reacting to your credit history and start shaping your credit future.

SECTION 2:

WHAT BANKS ACTUALLY LOOK AT

Lenders approve bankruptcy buyers based on risk reduction, not punishment.

They focus on:

Stable W-2 income (length matters more than amount)

Payment-to-income ratio

Time since filing or discharge

Down payment (even small helps)

Vehicle type & loan structure

📌 The goal isn’t perfection — it’s predictability.

Underwriting after a bankruptcy is essentially a “probability check” on whether your next loan will perform, which is why lenders lean into signals that reduce uncertainty and prove you can reliably carry the obligation going forward.

They typically view stable, documentable W-2 income as the strongest anchor—not because the dollar amount must be huge, but because length of employment and consistency of pay make your future payments easier to forecast.

From there, the payment-to-income fit is crucial: lenders want a structure that leaves breathing room after rent, utilities, insurance, and basic living expenses, because deals that run too tight are the ones that go late when life happens.

Timing since filing or discharge can help, but it’s often less important than whether your current profile shows a clean reset—no new unresolved issues and a realistic monthly budget.

Even a modest down payment can lower the bank’s exposure by improving equity and reducing the amount financed, while the vehicle choice and loan structure (year, mileage, reliability, term, and total amount financed) can either stabilize the deal or inject risk through repairs and rapid depreciation.

That’s why the goal isn’t perfection—it’s predictability: a loan that looks sustainable on paper and feels sustainable in real life, month after month.

SECTION 3:

CHAPTER 7 VS CHAPTER 13 — WHAT’S DIFFERENT?

Chapter 7:

Often eligible immediately after discharge

Faster approvals

Cleaner credit reset

Chapter 13:

May require trustee approval

Lenders focus heavily on income and payment history

Approval is common with proper structure

📌 Chapter 13 buyers are NOT denied — they’re just misunderstood.

The practical difference between Chapter 7 and Chapter 13 for car financing comes down to how lenders interpret “status” and control of the budget, not a blanket judgment about the person.

Chapter 7 is typically viewed as a completed reset once it’s discharged, which can make the approval conversation more straightforward because the court supervision is finished and the lender is underwriting a fresh post-discharge profile.

Chapter 13, however, is an active repayment plan, so the process often includes extra steps—sometimes trustee approval and a closer look at whether the proposed payment fits within the court-approved budget—meaning the buyer isn’t automatically riskier, just more regulated.

Because of that oversight, lenders tend to scrutinize income consistency and recent payment behavior more carefully, and they want a deal that clearly “fits” without creating stress or conflict with the plan.

When the structure is right—payment aligned with income, vehicle aligned with lender guidelines, and documentation handled cleanly—Chapter 13 approvals are often very achievable, and in many cases the presence of a documented plan can even reinforce the story that the borrower is on a disciplined path.

The issue is rarely denial—it’s misunderstanding the rules, the paperwork, and the structure needed to make the deal smooth.

SECTION 4:

WHAT VEHICLES MAKE APPROVAL EASIER

Banks prefer:

New vehicles under $30,000

Used vehicles 2020 or newer

Under 80,000 miles

Reliable brands with strong resale value

🚫 What to avoid:

High-mileage vehicles

Older luxury cars

“Too good to be true” payment ads

From an underwriting standpoint, the vehicle is the collateral that protects the loan, so lenders naturally gravitate toward units that are easier to value, easier to insure, less likely to break down, and more likely to retain enough market value over the life of the note.

That’s why approvals tend to come faster on reasonably priced new vehicles (often under a set ceiling like $30,000) and late-model used inventory—think 2020 or newer with under 80,000 miles—because those parameters reduce mechanical surprises and depreciation risk while keeping loan-to-value within guidelines.

Reliable brands with strong resale value matter because they lower the lender’s exposure if anything goes sideways, and they also lower the borrower’s ownership risk by limiting unexpected repair costs that can derail a payment plan.

On the flip side, high-mileage vehicles and older luxury cars can be approval killers not because they’re “bad cars,” but because they introduce higher repair probability, higher parts and maintenance costs, and weaker collateral protection, which makes the loan harder to justify.

And the “too good to be true” payment ads are often where people get trapped—those numbers frequently depend on unrealistic assumptions, heavy money down, or terms that don’t match the borrower’s profile—so the smartest move is to choose a lender-friendly vehicle first, then structure the deal around stability rather than chasing a headline payment.

SECTION 5:

HOW TO PROTECT YOURSELF FROM BAD DEALS

Before signing anything:

Ask for full numbers in writing

Understand the total loan amount

Confirm there are no hidden add-ons

Make sure the payment fits your long-term plan, not just today

📌 A good deal today that hurts you later isn’t a good deal.

The best protection is slowing the process down long enough to see the entire picture, because most “bad deals” don’t look bad in the showroom—they look convenient until the details show up later.

Start by insisting on a complete, itemized breakdown in writing so you can separate the vehicle price from taxes, fees, products, and any packages being bundled into the contract; when everything is transparent, you can actually evaluate value instead of reacting to a monthly payment.

Pay special attention to the total amount financed, because that number determines how long you’ll be upside down, how much interest you’ll pay over time, and how difficult it will be to refinance or trade if your situation changes.

Confirm exactly what’s included—and what’s optional—so you’re not quietly paying for add-ons you didn’t request or don’t need, especially when those products inflate the loan and slow your equity growth.

Finally, pressure-test the payment against your real-life budget and future goals: if the deal only works when nothing unexpected happens, it isn’t structured for success.

A good deal protects your next step—refinance, upgrade, lower rates—not just your ability to drive home today, because a deal that feels good now but limits you later was never a good deal in the first place.

SECTION 6:

THE SMART BUYER STRATEGY (STEP-BY-STEP)

1️⃣ Know your real budget, not the ad

2️⃣ Work with someone who specializes in bankruptcy buyers

3️⃣ Choose the right vehicle first

4️⃣ Structure the deal for approval

5️⃣ Use the loan as a credit rebuilding tool

This is how you turn a car purchase into a financial reset.

A smart bankruptcy buyer treats the purchase like a planned rebuild project instead of a reaction to an ad, because ads are designed to grab attention, not reflect your real approval or long-term cost.

The first step is setting a budget based on your actual monthly reality—income you can document, expenses you can’t avoid, and a payment that leaves room for insurance, maintenance, and life surprises—so the deal is stable even on a “normal” month.

From there, the fastest path is working with someone who understands bankruptcy approvals and lender guidelines, because specialization prevents trial-and-error submissions that waste time and add unnecessary inquiries.

Next, you pick a lender-friendly vehicle on purpose—one that fits year, mileage, price, and reliability standards—so the collateral supports the approval instead of fighting it.

Then you structure the deal to win: right term, realistic payment-to-income, appropriate down payment (if needed), and correct lender placement, so the loan is not only approved but built to perform.

Finally, you treat the loan as a tool—paying on time, avoiding new debt right away, and staying consistent—so the account becomes months of positive history that positions you for refinancing, better rates, and better options later.

That’s how a car purchase stops being a stressful transaction and becomes a true financial reset.

SECTION 7:

WHAT A GOOD ADVISOR SHOULD DO FOR YOU

A professional should:

Explain approvals clearly

Set expectations honestly

Offer multiple options

Protect your future credit

Never pressure you

If someone rushes you, avoids questions, or pushes fear — walk away.

A good advisor acts like a translator and strategist, not a closer—because your best outcome comes from understanding the path, not being pushed down it.

They should be able to break approvals down in plain language so you know why a lender is saying yes or no, what documentation matters, and what changes would improve the decision, instead of hiding behind vague phrases like “the bank won’t do it.”

Honest expectation-setting is essential: a professional tells you what’s realistic on rates, payments, and vehicle parameters today, and then maps out how you can improve those terms later, so you’re not sold a fantasy that turns into regret.

They should also present multiple workable options—different vehicles, structures, or lender directions—so you can choose what best fits your budget and goals rather than being boxed into a single deal that benefits the seller.

Most importantly, they protect your future credit by avoiding unnecessary submissions, preventing overreach, and making sure the loan is designed to succeed month after month, because your real win is what the deal does for you six to twelve months from now.

And if anyone tries to rush you, dodges direct questions, or uses fear to force urgency, that’s a warning sign: the right advisor earns trust through clarity, patience, and zero pressure, not through panic.

FINAL WORD:

YOUR BANKRUPTCY IS NOT YOUR IDENTITY

Bankruptcy is a chapter, not the story.

With the right guidance, the right structure, and the right mindset, this purchase can be the first step forward, not another setback.

Bankruptcy doesn’t define who you are—it defines what you’ve been through, and there’s a big difference.

It’s a legal process designed to restore stability, not a permanent label that follows you forever, and the moment you treat it like a life sentence is the moment you start making fear-based decisions.

The healthiest approach is to view your next financial move as a rebuild decision, not a recovery scramble: you’re proving reliability one month at a time, rebuilding confidence through consistent actions, and creating a paper trail that shows you can manage real obligations responsibly.

When you shift your mindset from “I hope someone approves me” to “I’m choosing the smartest path to strengthen my profile,” you stop feeling powerless and start steering the outcome.

That’s why the right guidance and structure matter so much—because the goal isn’t just getting into a vehicle, it’s protecting your momentum once you do.

A properly planned purchase aligns the payment with your actual life, reduces stress points that cause late payments, and sets you up for the next milestone—refinancing, upgrading, lowering interest, or expanding your credit options—without needing to start over again.

When the deal is built to perform and your habits stay consistent after delivery, that account becomes evidence of change that lenders can’t ignore.

Done correctly, this isn’t another setback you survive; it’s the first concrete step forward that helps you reclaim control of your finances and rewrite what happens next.

READY FOR YOUR PERSONAL ROADMAP?

If you’d like a private, no-pressure evaluation to see what options you qualify for, I’m happy to help.

📞 Call/Text: 614-377-7964

🌐 Website: columbuscarcredit.com

Dee Jones is an automotive sales leader, mentor, and industry contributor focused on developing high-performing professionals in retail automotive sales.

Call or text me directly at 614-377-7964, or connect with my partners at BizApp247, the leading AI-powered sales and marketing platform helping dealers and brokers across the Midwest build smarter, stronger, more connected businesses.